What Happens When Private-equity Firms Start Making Deals?

Private equity. The very term continues to evoke admiration, envy, and in the hearts of lots of public company CEOs fear. Recently, private equity companies have filched huge and controversial sums, while stalking ever bigger acquisition targets. Certainly, the global worth of private equity buyouts larger than $1 billion grew from $28 billion in 2000 to $502 billion in 2006, according to Dealogic, a firm that tracks acquisitions.

Private equity firms’ reputation for significantly increasing the worth of their financial investments has actually assisted fuel this development. Their capability to attain high returns is typically associated to a number of factors: high-powered rewards both for private equity portfolio managers and for the operating managers of services in the portfolio; the aggressive use of financial obligation, which offers funding and tax benefits; a determined concentrate on money circulation and margin improvement; and freedom from limiting public company policies. manager partner indicted.

That method, which embodies a mix of organisation and investment-portfolio management, is at the core of private equity’s success. Public companieswhich inevitably get businesses with the objective of hanging on to them and incorporating them into their operationscan beneficially discover or borrow from this buy-to-sell technique. To do so, they initially require to comprehend simply how private equity companies utilize it so successfully.

It doesn’t make sense when an obtained business will take advantage of crucial synergies with the buyer’s existing portfolio of businesses. It definitely isn’t the method for a business to profit from an acquisition whose primary appeal is its prospects for long-term natural development. Nevertheless, as private equity firms have actually revealed, the strategy is ideally suited when, in order to understand an onetime, brief- to medium-term value-creation chance, purchasers should take outright ownership and control.

It can also be discovered with companies that are undervalued since their potential isn’t easily obvious. In those cases, once the changes necessary to achieve the uplift in worth have actually been madeusually over a duration of two to six yearsit makes good sense for the owner to sell the company and move on to new chances.

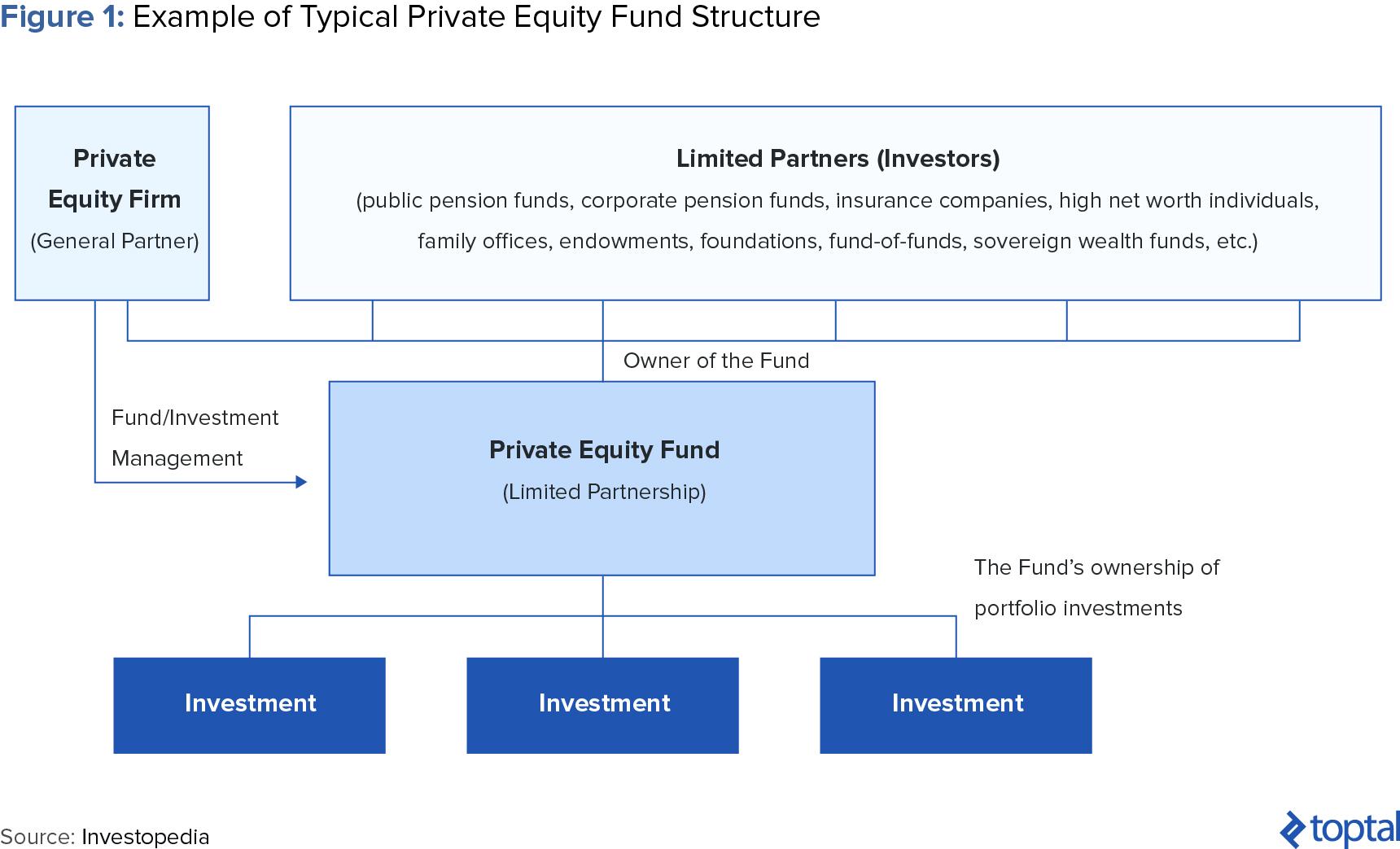

Particular funds can have their own timelines, investment objectives, and management approaches that separate them from other funds held within the very same, overarching management firm. Successful private equity firms will raise many funds over their life time, and as companies grow in size and intricacy, their funds can grow in frequency, scale and even specificity. To get more info regarding fund managers and - go to the websites and -.

Prior to founding Freedom Factory, Tyler Tysdal managed a growth equity fund in association with numerous stars in sports and home entertainment. Portfolio company Leesa.com grew quickly to over $100 million in incomes and has a visionary social objective to “end bedlessness” by donating one mattress for every ten sold, with over 35,000 contributions now made. Some other portfolio business remained in the markets of red wine importing, specialized lending and software-as-services digital signs. In parallel to managing possessions for services, Tyler Tysdal was managing private equity in real estate. He has had a number of effective private equity financial investments and several exits in trainee housing, multi-unit housing, and hotels in Manhattan and Seattle.

Private equity companies raise funds from institutions and rich people and after that invest that cash in purchasing and selling organisations. After raising a defined quantity, a fund will near to brand-new investors; each fund is liquidated, selling all its businesses, within a pre-programmed amount of time, generally no greater than ten years. securities fraud racketeering.

Private equity firms accept some restrictions on their usage of investors’ cash. A fund management agreement may limit, for example, the size of any single organisation financial investment. Once cash is devoted, however, investorsin contrast to shareholders in a public companyhave nearly no control over management (state prosecutors mislead). Although a lot of firms have an investor advisory council, it has far fewer powers than a public company’s board of directors.

Private Equity Marketing: The Complete Guide – Mediaboom

Instead, private equity firms work out control over portfolio companies through their representation on the companies’ boards of directors. Typically, private equity firms ask the CEO and other top operating managers of a company in their portfolios to personally buy it as a way to guarantee their dedication and motivation.

In accordance with this design, operating supervisors in portfolio businesses normally have greater autonomy than unit managers in a public business. Although private equity companies are beginning to develop operating abilities of their own and hence are now most likely to take an active role in the management of an obtained organisation, the conventional model in which private equity owners supply guidance however do not intervene straight in day-to-day operations still prevails.

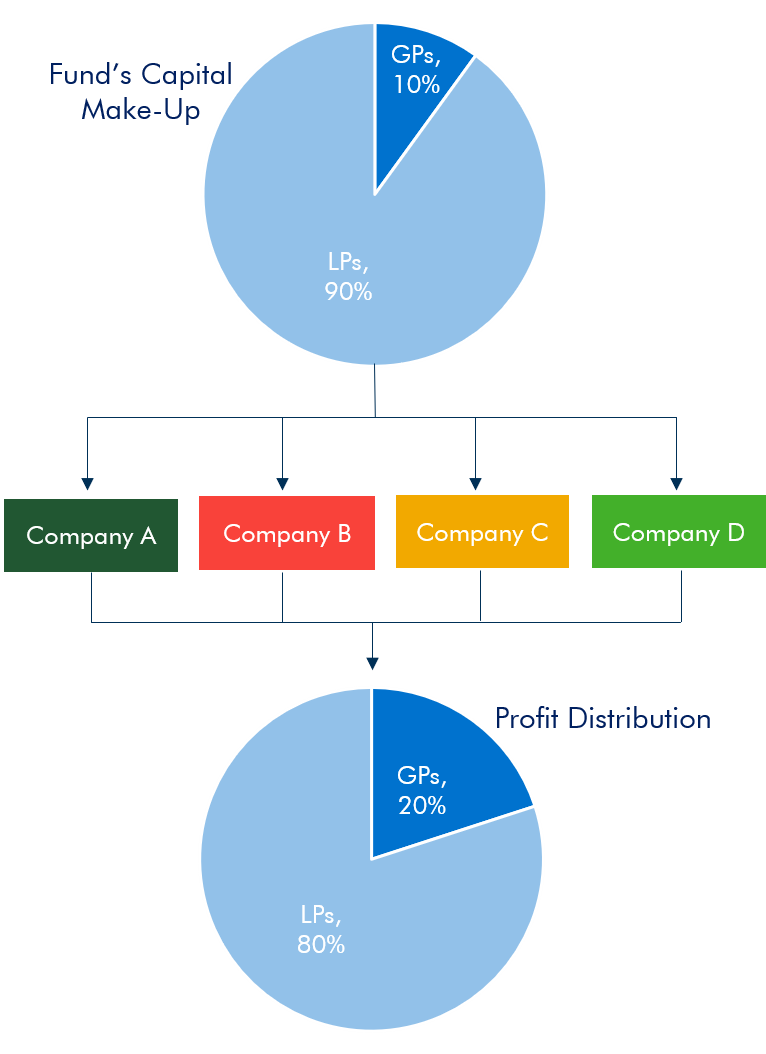

Fund revenues are primarily realized by means of capital gains on the sale of portfolio companies. Since funding acquisitions with high levels of debt improves returns and covers private equity firms’ high management costs, buyout funds look for out acquisitions for which high debt makes good sense. partner grant carter. To ensure they can pay financing expenses, they search for steady capital, minimal capital expense requirements, at least modest future growth, and, above all, the chance to boost performance in the brief to medium term.

In some countriesparticularly the United Statesthat provides essential tax and regulative benefits over public business. The advantages of purchasing to offer in such situations are plainthough, again, frequently neglected. Think about an acquisition that rapidly increases in valuegenerating an annual investor return of, say, 25% a year for the first three yearsbut consequently earns a more modest if still healthy return of, say, 12% a year.

A diversified public company that accomplishes identical operational efficiency with the acquired businessbut, as is normal, has purchased it as a long-lasting investmentwill earn a return that gets closer to 12% the longer it owns the organisation. For the general public company, hanging on to the service once the value-creating modifications have actually been made waters down the last return.

Under their previous owners, those organisations had actually frequently struggled with disregard, inappropriate efficiency targets, or other restrictions. Even if well handled, such organisations may have did not have an independent track record because the parent company had actually integrated their operations with those of other units, making business hard to value. Sales by public companies of unwanted service systems were the most crucial category of big private equity buyouts till 2004, according to Dealogic, and the leading companies’ commonly admired history of high investment returns comes mostly from acquisitions of this type.

( See the display “Private Equity’s New Focus.”) This has produced new difficulties for private equity firms. In public companies, quickly realized improvements in performance frequently have already been attained through much better business governance or the advocacy of hedge funds. For example, a hedge fund with a considerable stake in a public company can, without having to purchase the company outright, pressure the board into making important changes such as selling unnecessary assets or spinning off a noncore system.

What Do Private Equity Firms Say They Do? – Harvard …

When KKR and GS Capital Partners, the private equity arm of Goldman Sachs, obtained the Wincor Nixdorf system from Siemens in 1999, they were able to deal with the incumbent management and follow its plan to grow incomes and margins. On the other hand, because taking Toys “R” United States private in 2005, KKR, Bain Capital, and Vornado Real Estate Trust have had to replace the entire top management group and establish a whole brand-new technique for business.

And it might end up being harder for companies to cash out of their financial investments by taking them public; offered the present high volume of buyouts, the variety of big IPOs could strain the stock markets’ capability to soak up brand-new problems in a couple of years. Even if the current private equity investment wave declines, however, the distinct advantages of the buy-to-sell approachand the lessons it provides public companieswill stay – civil penalty $.

On the other hand, a business unit that has belonged to a public business’s portfolio for a long time and has carried out sufficiently, if not spectacularly, generally does not get priority attention from senior management. In addition, since every investment made by a private equity fund in a company need to be liquidated within the life of the fund, it is possible to precisely measure money returns on those financial investments (cobalt sports capital).

Tags: Tyler Tysdal

previous - next